Hey guys,

Today I want to walk you through my property journey.

At the time of writing all the deals are still in progress, so technically I own zero until I exchange.

Buying, getting the mortgage in principle, then the offer then exchanging will very rarely happen in 30 days.

The whole process based upon my limited experience to date is ball achingly slow.

However, what I want to do in this letter is walk you through one of these deals I’ve done and therefore how you can hopefully do some of your own as well.

Now to get ahead of any questions/fact/sense checking – all my experience is anecdotal.

I’m not a professional investor even if legally I’m classified as a portfolio landlord and professional investor.

I’m just a regular guy trying sh*t out on the basis of what people (on Google or in person) tell me is a smart thing to do.

So I just checked my account – as it stands I’ve got £263k in my Forex trading account.

Simply put, this is quite a lot of money to have in there.

It still remains the easiest but perhaps riskiest income generator that I have.

You can watch my trades here and if you want to learn more just email me back.

So then it made sense to start looking at more secure investments.

Truth is, I should have moved onto the property a long time ago but I find it somewhat boring.

Until I started to learn.

During the month of October 2019, I decided to dive deep into the property after my parents decided for me.

I’d had a bad experience with buying my first property an off-plan PBSA (purpose-built student accommodation) which I’ll come to in another email so was not ‘logically motivated’ to buy a place

I’d emotionally been stung by the Liverpudlian PBSA so just left if there.

However, that was until I got a phone call from my mum.

Now, my mum, mostly on Whatsapp messages me, and so if she calls me it’s somewhat of a big deal because it’s just damn unusual.

This case was no different.

‘Deepak how are you?’

I’m good mum how are you?

‘Dad and I -’

Her tone was different this time. She sounded almost excitable (very odd for my mum) and didn’t even respond to my question.

It was clear this was a call in which she had something specific to say.

‘Your dad and I saw a place on Cherry Tree Avenue on the bus home that had a for-sign sale – so we called the estate agent and have booked a viewing we think the place is perfect for you so we think you should buy it

Wow, that was a long sentence!

My mum had launched right into it without pausing to take a breath. She’d even called the estate agent, already made an appointment and wanted me to come and see the place.

One of the disappointments my parents had when I bought the place in Liverpool was that it was far away and so they couldn’t really be part of that experience.

It wasn’t a place that was close, in an area they knew about and something, therefore, they could be involved in.

I love my parents with all of my heart, and they had done everything for me to help me succeed and I still feel like I owe them everything.

My dad spends hours surfing Zoopla (once he got a smartphone) as well as looking at property in the local paper.

My dad, because he gave up his life for his children (which you can read about here) never got the opportunity to fulfil his own entrepreneurial ambitions – which I think came to life once he had time in his 50s to begin to think not about his children. But for himself.

(Blame that on me for not getting my act together for many years)

And so it was done.

At that moment, I knew I would be buying that place.

And once I was ‘emotionally’ invested, then I was fully in – come hell or high water.

That is just my style.

That’s where the journey began.

I went to visit this 1-bedroom apartment with a garage and a garden on the market for £220k in Yiewsley.

It was overpriced, so ultimately I was a little surprised when my offer of £205k was accepted.

Furthermore, in his later exhilaration, my estate agent unwittingly said to me ‘the buyer should be pleased – I told him ‘I just made you 15k!’.

So, in hindsight had I been more firm I probably could have gotten it down closer to 190k.

But this is how you learn :p

I went to view the property with my mum (my dad was at work) – I could tell as we walked over that it was her mission ‘show Deepak what a perfect place to buy this is!’.

And if my mum was invested it would ultimately mean my £70k would ultimately follow.

Now much like exams, I may have done some reading up historically on the property and got some advice here and there…but it seemed irrelevant to my situation and so I never did much with that advice.

It had all become quite forgettable.

But once I knew I was going to be throwing down (potentially) a very (for me!) memorable amount of money – my emotional levers kicked in and it was time to learn/execute.

So, ultimately here have been the things I’ve figured out in the few months I’ve been doing this.

Figure out what kind of investor you want to be.

Property Hub does a cracking job of describing this here (and it’s been through their platform that I’ve learnt a lot about a property)

For me, I want to generate enough cash flow to make a £10,000 salary from the property on a monthly basis (which makes me Income Ian according to the Property Hub model) that was passive.

I didn’t want to be fussed with flips, with refurbs, remodels or neutral/negative cash flow.

Property is, of course, a long-term investment – but I believe cash is king.

I believe in cash here and now; and then if I get a long-term return that’s a bonus!

So, then how can we achieve both perhaps?

Well, let’s talk in terms of gross figures to break it down with a DIFFERENT property I am purchasing.

The one above is still decent. The rent should be around £900. The mortgage is around £360.

Therein lies my scalp – £540 per month gross. Maybe brought down to £340 net.

But I’ll walk you through a deal I chose for myself rather than a deal that was chosen for me somewhat for better clarity:

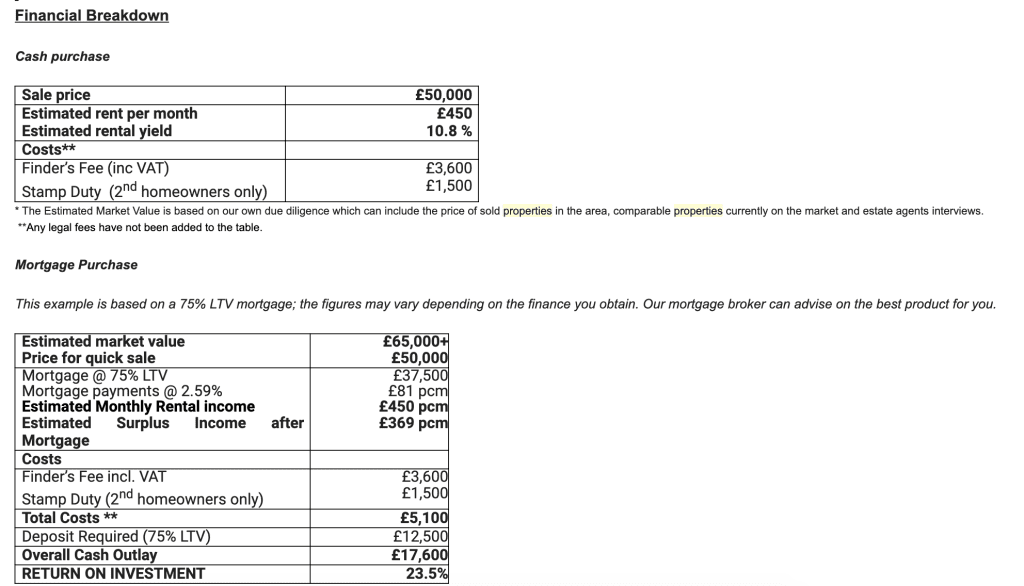

One of the properties I’m buying is costing me £50,000 excluding the £3,000 sourcing fees. (I’ll talk about my buying strategy in a little while)

Then you have solicitors, brokers, stamp duty and miscellaneous costs.

Here’s the financial breakdown of the deal:

I didn’t go for a cash buyer and instead have got a mortgage (tough to find on a 50k property but I have figured it out now).

(Buying in cash is a dumb way to spend money – I did this with the Liverpool PBSA – will share this in a separate letter).

Now as you can see the ROI here is listed at 23.5% which is amazing – if true.

And here lies a couple of issues some might have with this which I’ll address now

- The rent will end up being £400-425 I think.

- The estimated market value is probably not quite right – more like £57.5k, I’d wager.

- It doesn’t include solicitors/brokers’ fees

- It doesn’t include the 2k I’ll spend improving the property

- It doesn’t include taxes (income is personal/corporate it company)

- It doesn’t account for the implications if bought through an LTD or personal

- It doesn’t account for property repairs

- It doesn’t account for ground rent, gas and electricity certificates and more

Naturally, this will bring down the true net ROI

[convertful id=”197358″]

But there are (in terms of how I operate) some very important things about this that for me it’s important that everyone understands:

The numbers stack up such that regardless of the above the ROI still makes sense.

And this is the way that I like to do deals – that they bank enough of a return that you don’t have to sweat the smaller numbers.

In any deal you go into – if you have to count your pennies – you will never make your £££

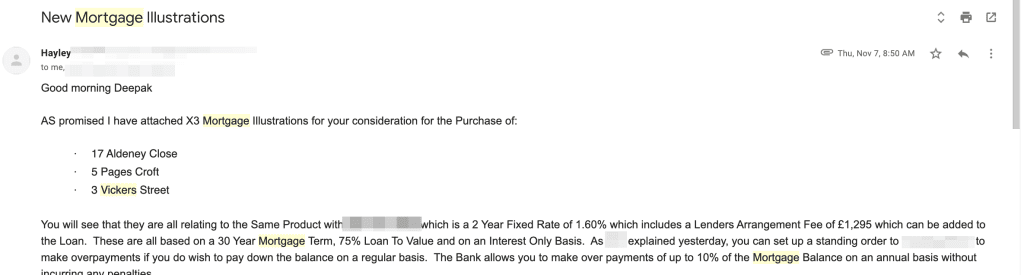

And there’s also a significant upside to this – I’ve actually got a mortgage rate of 1.69%:

Furthermore, as you might see at the bottom of the email – the plan I have (and I’m still thinking about it) is to maybe pay down the balance of 10% a year.

That would mean within 10 years I’ll own the property (probably smarter ways to ‘invest’ from this perspective but I love ‘owning’ sh*t LOL).

As of now, the bank will pretty much own it until they get paid off.

But my cash flow is (let’s say for argument’s sake) a net £300 (it’s £369 in their illustration so let’s knock off a decent amount to keep it easy) – and to achieve 10k a month I need to:

Divide £10,000 by the £300 net monthly income I’ll receive = 33.3x

This means I need to do a deal like this 34x to hit my 10k a month.

Let’s assume sh*t changes and it’s harder/longer etc and round up to 40x.

And that each deal costs me £20k all in to get it going.

40 x 20,000 = £800,000k

That’s the actual cash that I need to generate £120k per annum/£10k per month

Basically, for every £80k, I put in I get around £1k net back.

That on the surface of it seems like a lot of money.

BUT

- To hit a 5k cash flow I need £400k – and at that point, I could buy a new place every 4 months from the cash flow itself (5k x 4 = 20k).

- To hit a 4k cashflow I’d need £320,00k. Then I could buy every 5 months

- To hit a 3.5k cashflow I’d need £240k. Then I could buy every 6 months (I have this currently in Forex)

So really I need £240k to start making this become self-financing

And please note:

- All of this is without refinancing

- In a pretty ‘grim’ scenario – I’ve rounded up from 33.3 to 40 (that’s more than 100k!)

- And if we call this 18.5k instead of 20k it gets more interesting still

- Point 2 should account for bad tenants, costly repairs, unforeseen costs etc

Now this is one of several deals that I’m working on but is a good illustration of how I plan to ‘retire’

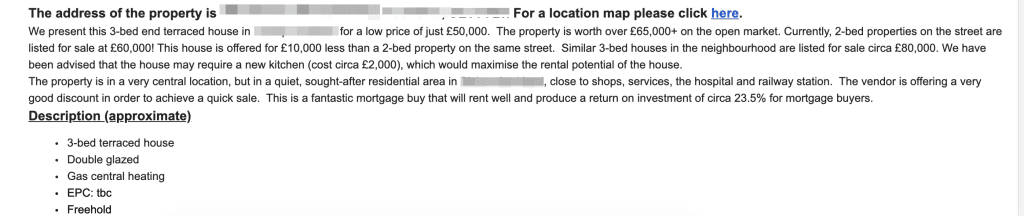

P.S here’s some more on the actual property itself further broken down.

So.

That’s some insight into how I try to find deals (and if you’re wondering this isn’t through Property Hub but I absolutely recommend them as a good learning resource).

I hope this has been insightful for you – and if you have any questions just let me know.

What I still find crazy is that YOU CAN, for around £20k, find properties on which an interest-only mortgage will cost you £70 a month and then you can rent the place out for around £400.

Crazy!

If you’d like to hear about the other ‘different’ types of deals I’ve done in property – just let me know